Dr. John Calabrese

Dr. John Calabrese

Teaches international relations at American University in Washington, DC. He is the book review editor of The Middle East Journal and a Non-Resident Senior Fellow at the Middle East Institute (MEI). He previously served as director of MEI’s Middle East-Asia Project (MAP). Follow him on X: @Dr_J_Calabrese

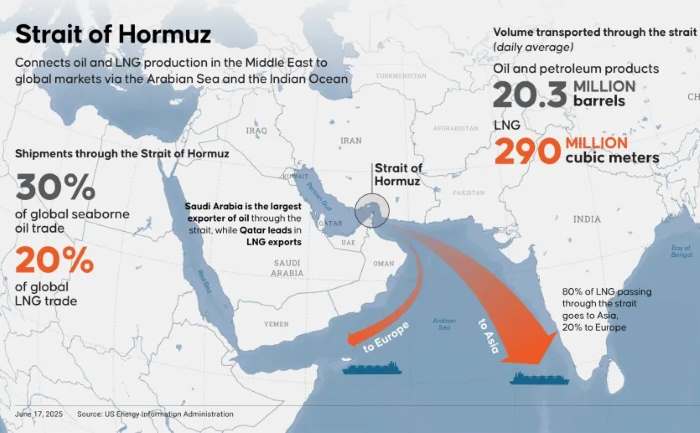

The U.S.–Israeli war with Iran has effectively closed the Strait of Hormuz, the corridor between Iran and Oman that carries roughly 20 percent of global oil and LNG. Within ten days, tanker flows halted, Brent crude surged toward $120 a barrel, and hundreds of vessels were delayed or rerouted. Since then, six vessels have come under attack in Gulf waters. In the first official statement attributed to him since assuming office, Iran’s new Supreme Leader, Mojtaba Khamenei, said Tehran would continue efforts to block the Strait.

The U.S.–Israeli war with Iran has effectively closed the Strait of Hormuz, the corridor between Iran and Oman that carries roughly 20 percent of global oil and LNG. Within ten days, tanker flows halted, Brent crude surged toward $120 a barrel, and hundreds of vessels were delayed or rerouted. Since then, six vessels have come under attack in Gulf waters. In the first official statement attributed to him since assuming office, Iran’s new Supreme Leader, Mojtaba Khamenei, said Tehran would continue efforts to block the Strait.

The impact of the closure will ultimately hinge on its duration. A disruption lasting days would be severe but manageable, while weeks could trigger cascading supply, price, and financial shocks. What had long been a tail risk has become reality, with uneven effects across producers, importers, and transit economies.

The Rerouting Calculus

The immediate question for Gulf producers has been whether alternative infrastructure can absorb the shock. The answer is partial and costly. Only Saudi Arabia and the United Arab Emirates (UAE) have operational pipelines bypassing the Strait, with combined capacity far short of the 20 million barrels that normally transit.

Saudi Arabia has activated its East–West Petroline, rerouting crude to the Red Sea port of Yanbu. Pakistan formally requested shipments be diverted through Yanbu, prompting Saudi assurances and at least one confirmed bypass delivery. Even at full capacity, these pipelines replace only a quarter to a third of normal Hormuz flows. In parallel, the International Energy Agency’s (IEA) member countries agreed to the largest emergency stock release in the agency’s history to alleviate immediate supply shortages.

The LNG outlook is more severe because it is harder to reroute. Qatar halted liquefaction at Ras Laffan Industrial City and Mesaieed Industrial City following Iranian drone strikes, declaring force majeure on exports and removing roughly one-fifth of global LNG supply almost overnight. Gas prices in Europe and Asia have surged roughly 65 percent, with the Japan Korea Marker jumping nearly 60 percent for April delivery. War-risk insurance premiums have also skyrocketed, reinforcing the shift to longer shipping routes.

Beneficiaries and Resilience

The disruption has produced a narrow but consequential set of beneficiaries. The most immediate is the United States. With Gulf production constrained and shipping through the Strait of Hormuz severely curtailed, the United States, the world’s largest oil exporter and LNG producer, finds its Atlantic-facing export routes insulated from the crisis.

Share prices of Cheniere Energy and Venture Global LNG, the two largest American LNG exporters, jumped in the week after Qatar’s production went offline. The structural asymmetry is striking: the U.S. imports only half a million barrels per day through the Strait, leaving it far less exposed than most major economies.

Secondary beneficiaries are emerging. With European markets scrambling to replace Qatari volumes, Russia has offered to resume long-term gas ties if Europe drops political preconditions. Australia also finds itself in an unexpectedly strong position, as its spare LNG capacity offsets a fifth of global seaborne supply now offline from the Gulf, creating a seller’s market for remaining exporters. Higher prices are also benefiting Atlantic Basin exporters such as Brazil and Guyana, whose crude can reach European and U.S. markets without transiting Middle Eastern chokepoints.

China has not proven to be the clear energy loser many analysts expected. Despite Gulf shipping disruptions, vessel-tracking data show Iran has sent at least 11.7 million barrels of crude to Chinese buyers since the war began. Tehran has also resumed tanker loading at the Jask terminal.

The longer-term beneficiaries may be those furthest along the energy transition. China plans to add roughly 200 GW of solar by 2027 for energy security, and India is accelerating solar deployment as part of its 300 GW capacity target by 2030. The crisis adds urgency to a supply-chain shift that was previously driven by climate policy, highlighting short-term resilience while accelerating transitions that will shape long-term market leverage.

The Cost of Gulf Energy Dependence

The burden falls most heavily on Asian economies whose industrial models were built on the assumption of cheap and reliable Gulf energy. India faces the region’s largest combined exposure. More than half of its LNG imports are Gulf-linked and a significant share is indexed to Brent crude, meaning a spike driven by disruption in the Strait of Hormuz simultaneously raises both oil import costs and LNG contract prices.

South Asia more broadly is acutely vulnerable. Pakistan sources nearly 99 percent of its LNG imports from Qatar, and Bangladesh sources around 70 percent. Bangladesh has ordered university closures and introduced fuel rationing as its energy crisis deepens, turning to costly spot-market LNG purchases to cover supply gaps. Pakistan has imposed more than a dozen austerity measures, including halving the government workforce, adopting a four-day workweek, cutting fuel allocations for official vehicles, banning iftar gatherings, and closing schools for two weeks.

Southeast Asia occupies a middle ground. Thailand, Vietnam, and the Philippines rely on imported LNG and Gulf crude but also receive shipments from Australia and Malaysia. Fuel costs in these countries are already pushing up electricity prices and inflation.

Japan and South Korea, though better stocked than South Asia, face severe LNG price exposure. Japan holds roughly 4 million tons of LNG, about a three weeks’ supply, while South Korea exceeds its 9-day minimum stockpiling requirement. Nevertheless, South Korea remains particularly vulnerable, sourcing around 70 percent of its oil from the Middle East, predominantly from Gulf producers.

Beyond Asia’s advanced economies, developing countries face the greatest risks. South Asian LNG buyers, constrained by limited foreign-exchange reserves and subsidized power markets, are highly exposed to price spikes. Pakistan canceled LNG tenders in 2019 and 2025, and Bangladesh did so in 2020. These shocks compound inflation, currency pressures, and fiscal stress across energy-dependent economies.

Systemic Fragility

What the Hormuz closure has exposed is not merely a supply disruption but a fundamental divergence in economic resilience. Unlike previous Gulf disruptions—from the 1973 oil embargo to the 2019 attack on Abqaiq—the current crisis has halted not just production but the transit corridor itself, striking at the logistical heart of the global energy system.

The shock hits hardest where energy import dependence is highest and hedging capacity is lowest. It hits least where domestic production is highest, supply diversification most advanced, or where the pivot to renewables furthest along. Bernstein analysts warn that a prolonged disruption could push oil to $120–$150 per barrel, with demand destruction at $155. At these levels, inflationary and recessionary pressures on energy-dependent developing economies are existential.

Critically, a formal reopening of the Strait would not bring immediate relief to the most exposed economies. Backlogged vessels, elevated war-risk insurance premiums, and disrupted supply contracts could take weeks or months to normalize. The resulting delays may prolong price and supply stress while highlighting the need for coordinated policy responses, including strategic reserve releases and targeted subsidies.

Structural Realignment

The deeper question is whether the disruption will permanently reshape global energy trade. Use of the Cape of Good Hope route, which adds roughly 15 days and $3–5 million per voyage, has again become the default detour away from Middle Eastern chokepoints.

Meanwhile, the Nigeria–Morocco Gas Pipeline—a 5,660-km project linking Nigerian gas fields to Europe through 13 West African states—has gained renewed strategic relevance since the Strait’s closure. The UAE joining the European Investment Bank, Islamic Development Bank, and OPEC Fund for International Development last May signals Gulf capital hedging against the chokepoint risks the crisis has exposed.

The disruption is reshaping maritime logistics. Gulf hubs, including Fujairah, Ras Tanura, and Jebel Ali, have stalled, while alternative gateways like Yanbu, Rotterdam, and Singapore absorb rerouted cargoes. Even if the Strait reopens soon, shipping is unlikely to return quickly to pre-crisis patterns. Vessel repositioning and insurance normalization, along with the renegotiation of contracts disrupted by force majeure, could extend the disruption for months. Prolonged instability may also leave lasting effects, reshaping tanker routes and altering port competitiveness.

More broadly, an eventual reopening would still underscore the vulnerability of routing roughly a fifth of global oil and gas through a single chokepoint. Gulf producers are likely to expand bypass infrastructure, while Asian importers may diversify supply relationships. The crisis thus tests a longstanding geopolitical assumption: that routing a large share of global energy through a single chokepoint is an acceptable trade-off for access to relatively cheap hydrocarbons. In that sense, the Hormuz shock has done more than raise prices. It has exposed the fragility of the world’s most important energy corridor and redrawn the map of who is exposed, who is insulated, and who will wield leverage to shape the energy order.

Courtesy : Gulf International Forum / Featuring Map Figures from the year 2024

{kind=link}